Introduction

Industrial starch is a carbohydrate-based material derived from agricultural feedstocks such as corn, wheat, potatoes, cassava, and other crops. It consists of long chains of glucose molecules and serves as one of the most important bio-based raw materials used across multiple industries. Through physical, chemical, and enzymatic modification processes, starch can be tailored to deliver specific characteristics including viscosity, stability, gelatinization behavior, water retention, and binding properties. These functional attributes have enabled industrial starch to establish a strong presence across food and beverages, paper and packaging, pharmaceuticals, textiles, personal care products, adhesives, animal feed, and biodegradable plastics.

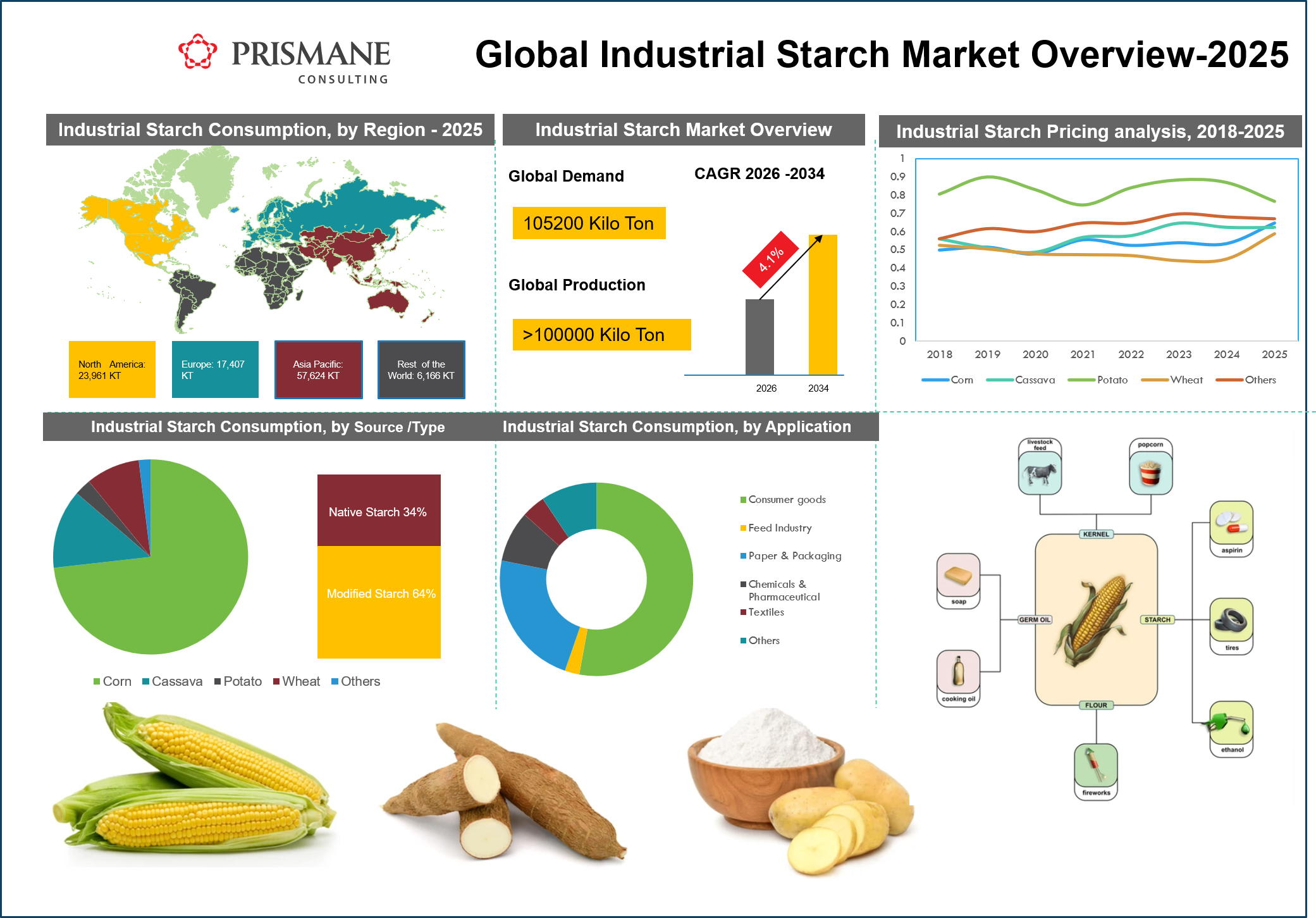

Market Overview

The global industrial starch market represents a high-volume industry with annual consumption estimated at around 105 million tons. Market growth is supported by increasing processed food consumption, rising investments in pharmaceutical manufacturing, expansion of the paper and packaging industry, and growing demand for sustainable materials. Modified starch constitutes the fastest-growing product category owing to its superior functionality and higher value addition compared with native starch. Demand for modified starch is projected to grow at a faster pace as manufacturers increasingly focus on customized ingredients capable of delivering improved performance across diverse applications.

Supply Scenario and Production Capacity

The industrial starch industry is supported by substantial production capacities concentrated in major agricultural economies. China remains one of the largest producers and consumers globally, benefiting from abundant corn supplies and extensive wet milling infrastructure. The United States also occupies a leading position in the global market due to its large corn production base, advanced processing technologies, and integrated supply chains. Europe, particularly France, Germany, and the Netherlands, maintains significant starch production capacities based on wheat, corn, and potato feedstocks. Thailand and Indonesia dominate the global tapioca starch supply chain, supported by strong cassava cultivation and competitive manufacturing economics. India has also emerged as an important producer, with increasing investments aimed at meeting growing domestic demand from food processing, pharmaceuticals, textiles, and paper industries.

Demand-Supply Dynamics

Global industrial starch demand continues to exhibit stable growth supported by favorable demographic trends and increasing industrial applications. Rising urbanization, growing disposable incomes, and changing consumer preferences have accelerated demand for convenience foods and packaged products, thereby increasing starch consumption. Expansion of pharmaceutical manufacturing, growth in e-commerce-driven packaging demand, and rising investments in sustainable materials have further strengthened market fundamentals. Although supply conditions remain relatively balanced, fluctuations in agricultural commodity prices, adverse weather conditions, and geopolitical developments can periodically impact feedstock availability and manufacturing economics.

Regional Analysis

Asia Pacific accounts for more than 50% of global industrial starch consumption and remains the largest regional market. Strong industrialization, expanding middle-class populations, rising spending power, and rapid growth in food processing industries have transformed the region into the center of global starch demand. Countries such as China, India, Japan, South Korea, Indonesia, and Thailand collectively account for a substantial share of worldwide consumption. Continuous investments in production capacities and downstream value-added products are expected to further strengthen the region's leadership position.

North America represents a mature market characterized by advanced technologies and strong production capabilities. The region benefits from abundant corn availability and a well-established supply chain. Europe continues to focus on specialty and modified starch products while increasing emphasis on sustainability and clean-label ingredients is encouraging innovation across the industry.

Product Segment Analysis

Corn starch remains the dominant segment owing to its cost competitiveness and widespread availability. The United States, China, and Europe collectively account for a significant portion of global corn starch production capacity. Tapioca starch has witnessed robust demand growth due to increasing preference for gluten-free ingredients and broader industrial applications. Thailand and Indonesia remain the leading producers and exporters of tapioca starch. Wheat starch continues to enjoy strong demand across Europe, while potato starch occupies an important position in food processing and industrial applications due to its superior viscosity and water-binding characteristics.

The global industrial starch market is broadly categorized into two primary product types: native (or conventional) starch and modified starch. Currently, modified starch dominates the market landscape, commanding a substantial share of around 64%, while native starch holds the remaining approximate 34%. This significant margin underscores the growing industrial preference for starches that have been physically, enzymatically, or chemically altered to exhibit enhanced functional properties.

Modified starches are increasingly favored across a wide range of end-use industries including food and beverage, papermaking, textiles, pharmaceuticals, and adhesives due to their superior characteristics such as improved stability under high temperatures, better freeze-thaw resistance, enhanced thickening and binding capabilities, and longer shelf life. These attributes make them indispensable in processed foods, convenience meals, and industrial applications where native starches would otherwise fall short in performance.

Conversely, native starch continues to maintain a steady, though smaller, share of the market, primarily driven by its cost-effectiveness and its use in traditional applications such as direct food thickening, dusting powders, and certain paper-coating processes. However, its growth is relatively muted compared to modified starch, as it lacks the versatility required for modern, high-performance industrial processes.

Looking ahead, the escalating demand for modified starch is expected to act as a primary catalyst for the overall industrial starch market during the forecast period. Several key factors are fueling this upward trajectory:

- Rising processed food consumption: Rapid urbanization and changing dietary habits, particularly in emerging economies, are boosting the need for convenience foods that rely heavily on modified starch as a texturizer and stabilizer.

- Growth in pharmaceutical and personal care sectors: Modified starches are increasingly used as excipients in tablet formulations and as binders in cosmetics, further expanding their application scope.

- Sustainability and bio-based trends: As industries shift away from synthetic chemicals toward renewable, biodegradable raw materials, modified starch offers a functional and eco-friendlier alternative in products like biodegradable plastics and eco-friendly adhesives.

- Technological advancements: Continuous R&D efforts are leading to the development of novel modified starch variants with specialized properties, opening new opportunities in niche applications such as clean-label foods and high-performance drilling fluids.

As a result, the sustained growth in the modified starch segment is projected to significantly propel the entire industrial starch market forward, offsetting the relatively slower expansion of the native starch segment. This momentum is expected to be particularly pronounced in Asia-Pacific and Latin America, where rapid industrialization and increasing disposable incomes are driving robust demand across multiple downstream industries.

Application Analysis

Food and beverage applications account for the largest share of industrial starch consumption. Starch functions as a thickening agent, stabilizer, emulsifier, and texture enhancer in sauces, soups, bakery products, confectionery, dairy products, and processed foods. Rising demand for convenience foods and premium packaged products continues to support market expansion.

The paper and packaging sector constitutes another major end-use industry where starch is utilized in surface sizing and coating applications to improve paper strength, printability, and ink absorption. Growth in e-commerce activities and increasing demand for sustainable packaging solutions are creating favorable conditions for starch consumption.

Pharmaceutical manufacturers rely on starch as an essential excipient for tablet binding, disintegration, and controlled-release formulations. Textile manufacturers use starch-based sizing agents to improve weaving efficiency and fabric quality. Increasing environmental concerns and regulatory pressure on conventional plastics are also accelerating investments in starch-based biodegradable materials, making bioplastics one of the fastest-growing application segments.

Trade Analysis

International trade plays an important role in balancing regional demand and supply. Major exporting countries include the United States, Thailand, Indonesia, China, France, and the Netherlands. Trade flows are influenced by agricultural production, freight rates, exchange rate fluctuations, tariffs, and geopolitical developments. Supply chain disruptions resulting from the Russia-Ukraine conflict and elevated logistics costs have affected global trade patterns and increased price volatility across several regions.

Price Trend and Cost Structure

Industrial starch production economics are primarily influenced by feedstock prices, energy costs, transportation expenses, labor charges, and currency movements. Corn, wheat, and cassava prices have a direct impact on production costs, while fluctuations in energy markets influence utility and logistics expenses. Historically, industrial starch prices have ranged between USD 0.4 and USD 0.8 per kilogram. Inflationary pressures, rising agricultural commodity prices, geopolitical uncertainties, and increasing energy costs have supported an upward price trend. Modified and specialty starches generally command higher margins owing to their superior performance characteristics and greater value addition.

Competitive Landscape

The market is moderately consolidated with leading manufacturers focusing on capacity expansions, technological advancements, and portfolio diversification. Major participants include Cargill Incorporated, Archer Daniels Midland, Ingredion Incorporated, Tate & Lyle PLC, Roquette Frères, Tereos Group, AGRANA Beteiligungs AG, Avebe, Emsland Group, and Grain Processing Corporation. Companies are increasingly investing in specialty starches, clean-label ingredients, and sustainable solutions to enhance profitability and strengthen their competitive positions.

Future Outlook

The long-term outlook for the industrial starch market remains favorable. Rising food consumption, increasing packaging requirements, growing pharmaceutical production, and expanding investments in sustainable materials are expected to support market growth over the forecast period. Capacity additions across Asia Pacific, technological advancements in starch modification, and increasing adoption of bio-based chemicals are likely to enhance industry profitability and strengthen demand fundamentals. As sustainability initiatives and circular economy principles continue to gain momentum, industrial starch is expected to play a vital role in replacing conventional petroleum-based materials and creating new growth opportunities across multiple industries.